The Mighty Greenback

When the Australian Dollar (AUD) de coupled from the British pound in 1967 – just a year after the dollar itself was introduced sixty years ago this month – Australia began its long‑running obsession with the US Dollar (USD) as the reference point for valuing stuff we produced and stuff we wanted.

And it wasn’t just us down in the antipodes. Across the globe, trade invoicing increasingly shifted toward the USD, especially for commodities, and global capital flows followed suit. By the time the AUD was floated in 1983, the USD was the financial equivalent of a gorilla in a cuddly animal farm.

For everyday Australians, this meant the nightly news becamea financial scoreboard. Pride when the AUD/USD went up, panic when it went down (particularly for those dreaming of overseas holidays or a new Sony Walkman). Exporting farmers, of course, preferred the opposite – nothing like a falling AUD to make pool payments pleasantly plump.

But here’s the odd bit: Australia didn’t trade with the United States nearly as much as it traded with Asia (and still doesn’t). Did it really matter what the AUD/USD was doing?

Actually, yes. Most Asian currencies were either formally pegged to the USD or actively managed to shadow it. If the AUD fell against the USD, it generally fell against the RMB, the Baht, the Ringgit, and the rest of the neighbourhood. The USD was a very handy proxy for everywhere that wasn’t here - and being the world’s most traded, liquid, and stable currency - the classic “safe haven.”

At least until 2025.

The past year of US tariffs and geopolitical chest‑thumping has hastened a trend that’s been building for two decades. Currencies have been progressively de‑pegging from the USD, and some countries (China most notably) have been actively encouraging trade invoicing in their own currency. With the current US administration swinging haymakers at its largest trading partners, global trust in America’s willingness to act in the collective interest has been crushed faster than a Coke can on the Mitchell Freeway.

Confidence in the USD’s stability is also wobbling. Some in the current US administration openly want a weaker USD, others insist on a strong one, and the rest appear to be consulting a Magic 8‑Ball. That uncertainty makes investors nervous, and parking spare cash in US financial markets is no longer considered as safe as it was.

What This Means for Agriculture

If this trend continues, the field of play could shift in several ways:

1) Pricing Fragmentation

As more trade is denominated in multiple currencies rather than just USD we could expect:

2) Rise of Currency‑Dominated Trading Blocs

The EU is the poster child, but BRICS and South America’s Mercosur are continuing to explore how to get some distance from the US. Southeast Asia could drift the same way. The more Australia’s trading partners align into blocs, the weaker Australia becomes in negotiating power—think tariffs, quotas, and other fun barriers. (Here is a wild idea, maybe a new Commonwealth should get back together? Canada, Australia, UK and NZ are all desperate and bloc-less at the moment).

The counter‑trend—large powers like the US or Russia trying to break up competing blocs—brings its own risks, including more trade wars and the occasional hot one.

3) More Complex Financial Risk Management

Hedging on CBOT works partly because so many traders do and, because it’s denominated in USD. If global trade shifts toward the Euro or RMB, liquidity could migrate to other exchanges. Australian exporters may need to juggle more hedging instruments across more markets. It’s financial risk management meets Cirque du Soleil.

4) Niche Opportunities

A fragmented system creates cracks where nimble operators can thrive. For example, an Australian agricultural trader importing Chinese fertiliser and exporting barley back to China could run a simple contra arrangement with a Chinese counterparty—lowering transaction costs, reducing FX risk, and embedding a relationship beyond spot pricing.

Where to from here?

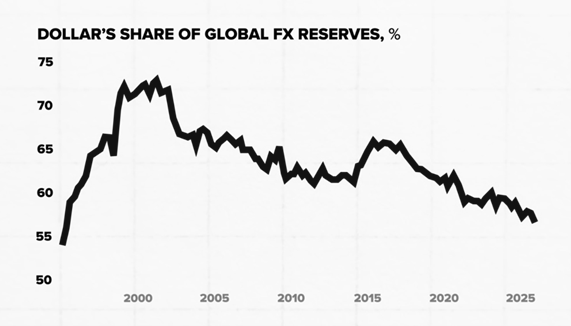

Although change is happening, the USD is still involved in 89% of global FX transactions (2025 numbers according to that frenzied mob of hedonistic party-goers - the Bank for International Settlements). Processes as intertwined as a tree trunk that enveloped a star picket don’t change overnight. But the geopolitical motivation to diversify away from the USD is stronger than ever – just ask Canada, Mexico, China, Brazil, all of Europe …you get the drift.

A multipolar world will bring pain from change but, for a small, agile island nation like Australia, it might just open more doors than it closes.